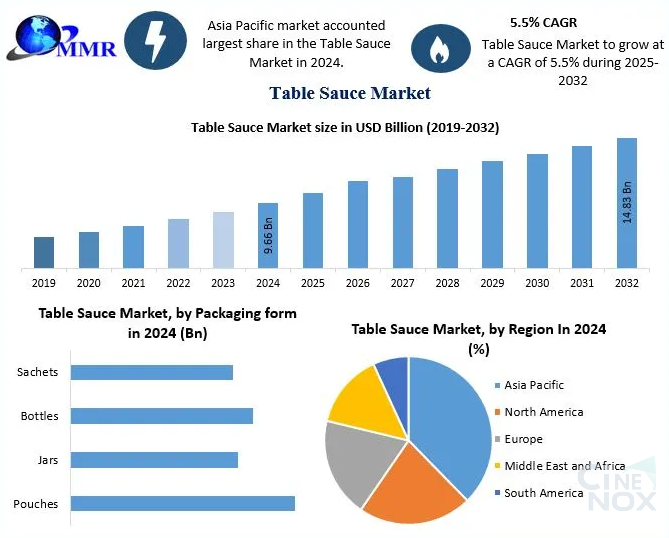

The Global Table Sauce Market is experiencing robust growth, driven by evolving consumer preferences, the rising popularity of ethnic and global cuisines, and increasing demand for convenience in meal preparation. Valued at USD 9.66 Billion in 2024, the market is projected to reach nearly USD 14.83 Billion by 2032, registering a CAGR of 5.5% during the forecast period (2025–2032).

Intrigued to explore the contents? Secure your hands-on sample copy of the report:

https://www.maximizemarketresearch.com/request-sample/32416/

Market Overview

Table sauces have become an integral part of modern dining, not only enhancing the taste of everyday meals but also providing visual appeal to dishes. Urban households increasingly keep a variety of sauces stocked at home, including soy sauce, tomato ketchup, mayonnaise, salad dressings, hot sauces, BBQ sauces, and ethnic varieties. These sauces are available in multiple forms such as liquid, solid, and cream, allowing consumers to complement any cuisine or dish.

Intrigued to explore the contents? Secure your hands-on sample copy of the report:

https://www.maximizemarketresearch.com/request-sample/32416/

Key Market Trends

1. Health and Wellness:

2. Ethnic and Global Cuisines:

3. Convenience Packaging:

4. Sustainability:

Key Market Segments

By Type:

Tomato Ketchup: Leading the market with a revenue of approximately USD 31.44 Billion in 2024, ketchup remains a staple in fast-food consumption, sandwiches, and fries. Its versatility also allows it to serve as a base for other sauces.

Mayonnaise: Popular in salads, sandwiches, and dressings, the segment is witnessing steady growth due to increasing consumer preference for creamy condiments.

By Packaging Form:

Pouches: Most popular form in 2024, accounting for 34.8% of market share.

Bottles & Jars: Traditional packaging for sauces, particularly for premium and artisanal products.

Sachets: Rapidly gaining traction for single-serve convenience, especially in quick-service restaurants and fast-food outlets.

By Distribution Channel:

Supermarkets & Hypermarkets: Leading distribution channels due to wide product selection and consumer access.

Intrigued to explore the contents? Secure your hands-on sample copy of the report:

https://www.maximizemarketresearch.com/request-sample/32416/

Regional Outlook

Asia Pacific:

The market in Asia Pacific is expected to grow at a CAGR of 7.1%, driven by an expanding fast-food sector, increasing disposable incomes, and the growing demand for convenience foods. China plays a significant role in production efficiency, while Western-style sauces are gaining popularity in urban cuisines.

North America:

North America is projected to witness a CAGR of 6.7%, with the U.S. market contributing a substantial share. Factors such as interest in international cuisines, health-oriented sauces, and government initiatives promoting diversified diets are fueling growth.

Europe:

Europe demonstrates steady growth owing to strong consumer awareness of quality, health, and premium food products. Countries like the UK, Germany, and France are major contributors, with a rising inclination toward gluten-free and organic sauces.

Leading Brands and Products

Prominent players driving the global table sauce market include:

Nestlé India

Everest Beverages & Food Industries

Heinz Wattie’s Ltd.

Del Monte Foods, Inc.

Levi Roots Reggae Reggae Foods Ltd

GB Sauce

Encona Sauces

The Great British Sauce Company

Clorox

McCormick & Company, Inc.

PepsiCo

Unilever

Hunt’s

Northwest Gourmet Foods

Orkla ASA

ACH Food Companies, Inc.

Contact Maximize Market Research:

MAXIMIZE MARKET RESEARCH PVT. LTD.

⮝ 3rd Floor, Navale IT park Phase 2,

Pune Banglore Highway, Narhe

Pune, Maharashtra 411041, India.

✆ +91 9607365656

🖂 sales@maximizemarketresearch.com

About Maximize Market Research:

Maximize Market Research is one of the fastest-growing market research and business consulting firms serving clients globally. Our revenue impact and focused growth-driven research initiatives make us a proud partner of majority of the Fortune 500 companies. We have a diversified portfolio and serve a variety of industries such as IT & telecom, chemical, food & beverage, aerospace & defense, healthcare and others.

The Global Table Sauce Market is experiencing robust growth, driven by evolving consumer preferences, the rising popularity of ethnic and global cuisines, and increasing demand for convenience in meal preparation. Valued at USD 9.66 Billion in 2024, the market is projected to reach nearly USD 14.83 Billion by 2032, registering a CAGR of 5.5% during the forecast period (2025–2032).

Intrigued to explore the contents? Secure your hands-on sample copy of the report: https://www.maximizemarketresearch.com/request-sample/32416/

Market Overview

Table sauces have become an integral part of modern dining, not only enhancing the taste of everyday meals but also providing visual appeal to dishes. Urban households increasingly keep a variety of sauces stocked at home, including soy sauce, tomato ketchup, mayonnaise, salad dressings, hot sauces, BBQ sauces, and ethnic varieties. These sauces are available in multiple forms such as liquid, solid, and cream, allowing consumers to complement any cuisine or dish.

Intrigued to explore the contents? Secure your hands-on sample copy of the report: https://www.maximizemarketresearch.com/request-sample/32416/

Key Market Trends

1. Health and Wellness:

2. Ethnic and Global Cuisines:

3. Convenience Packaging:

4. Sustainability:

Key Market Segments

By Type:

Tomato Ketchup: Leading the market with a revenue of approximately USD 31.44 Billion in 2024, ketchup remains a staple in fast-food consumption, sandwiches, and fries. Its versatility also allows it to serve as a base for other sauces.

Mayonnaise: Popular in salads, sandwiches, and dressings, the segment is witnessing steady growth due to increasing consumer preference for creamy condiments.

By Packaging Form:

Pouches: Most popular form in 2024, accounting for 34.8% of market share.

Bottles & Jars: Traditional packaging for sauces, particularly for premium and artisanal products.

Sachets: Rapidly gaining traction for single-serve convenience, especially in quick-service restaurants and fast-food outlets.

By Distribution Channel:

Supermarkets & Hypermarkets: Leading distribution channels due to wide product selection and consumer access.

Intrigued to explore the contents? Secure your hands-on sample copy of the report: https://www.maximizemarketresearch.com/request-sample/32416/

Regional Outlook

Asia Pacific:

The market in Asia Pacific is expected to grow at a CAGR of 7.1%, driven by an expanding fast-food sector, increasing disposable incomes, and the growing demand for convenience foods. China plays a significant role in production efficiency, while Western-style sauces are gaining popularity in urban cuisines.

North America:

North America is projected to witness a CAGR of 6.7%, with the U.S. market contributing a substantial share. Factors such as interest in international cuisines, health-oriented sauces, and government initiatives promoting diversified diets are fueling growth.

Europe:

Europe demonstrates steady growth owing to strong consumer awareness of quality, health, and premium food products. Countries like the UK, Germany, and France are major contributors, with a rising inclination toward gluten-free and organic sauces.

Leading Brands and Products

Prominent players driving the global table sauce market include:

Nestlé India

Everest Beverages & Food Industries

Heinz Wattie’s Ltd.

Del Monte Foods, Inc.

Levi Roots Reggae Reggae Foods Ltd

GB Sauce

Encona Sauces

The Great British Sauce Company

Clorox

McCormick & Company, Inc.

PepsiCo

Unilever

Hunt’s

Northwest Gourmet Foods

Orkla ASA

ACH Food Companies, Inc.

Contact Maximize Market Research:

MAXIMIZE MARKET RESEARCH PVT. LTD.

⮝ 3rd Floor, Navale IT park Phase 2,

Pune Banglore Highway, Narhe

Pune, Maharashtra 411041, India.

✆ +91 9607365656

🖂 sales@maximizemarketresearch.com

About Maximize Market Research:

Maximize Market Research is one of the fastest-growing market research and business consulting firms serving clients globally. Our revenue impact and focused growth-driven research initiatives make us a proud partner of majority of the Fortune 500 companies. We have a diversified portfolio and serve a variety of industries such as IT & telecom, chemical, food & beverage, aerospace & defense, healthcare and others.