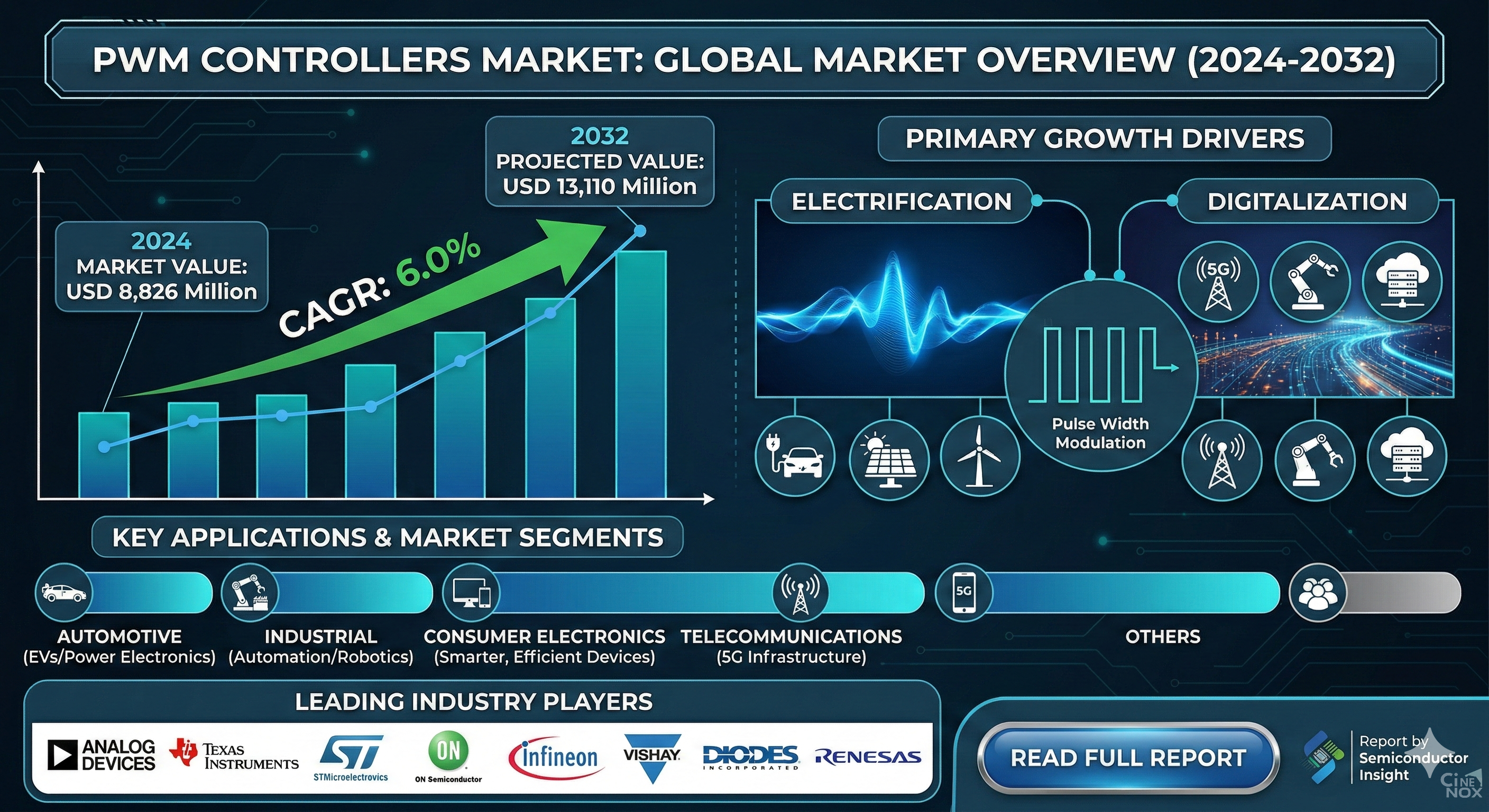

Global PWM Controllers Market Set to Reach USD 13.1 Billion by 2032, Driven by Electrification and Digitalization Trends

The global Pulse Width Modulation (PWM) Controllers Market is positioned for steady growth, projected to rise from USD 8.8 billion in 2024 to USD 13.1 billion by 2032, reflecting a CAGR of 6.0%. According to a report by Semiconductor Insight, this expansion is primarily fueled by the twin forces of global electrification and digitalization.

PWM controllers are essential silicon components that regulate power delivery with high efficiency by rapidly switching current on and off. Their ability to minimize heat loss while providing precise voltage control makes them indispensable in the modern transition toward energy-conscious technology.

Key Market Highlights:

Primary Drivers: The shift toward Electric Vehicles (EVs), the rollout of 5G telecommunications, and the rise of intelligent industrial automation.

Leading Segments: Current Mode Controllers and Industrial Applications currently dominate the market landscape.

Technology Trends: There is a growing shift toward integrating PWM functionality into System-on-Chip (SoC) designs and developing controllers with higher switching frequencies to allow for smaller overall device footprints.

Competitive Landscape: Industry leaders include Texas Instruments, Analog Devices, STMicroelectronics, Infineon, and ON Semiconductor, all of whom are focusing on geographic expansion into the high-growth Asia-Pacific region.

Get Full Report Here: Pulse Width Modulation (PWM) Controllers Market, Global Business Strategies 2025-2032 - View in Detailed Research Report

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=122483

#Semiconductors #PWMControllers #PowerManagement #TechTrends2026 #ElectricVehicles #DigitalTransformation #EnergyEfficiency #IndustrialAutomation #ElectronicsIndustry #MarketResearch #SemiconductorInsight

The global Pulse Width Modulation (PWM) Controllers Market is positioned for steady growth, projected to rise from USD 8.8 billion in 2024 to USD 13.1 billion by 2032, reflecting a CAGR of 6.0%. According to a report by Semiconductor Insight, this expansion is primarily fueled by the twin forces of global electrification and digitalization.

PWM controllers are essential silicon components that regulate power delivery with high efficiency by rapidly switching current on and off. Their ability to minimize heat loss while providing precise voltage control makes them indispensable in the modern transition toward energy-conscious technology.

Key Market Highlights:

Primary Drivers: The shift toward Electric Vehicles (EVs), the rollout of 5G telecommunications, and the rise of intelligent industrial automation.

Leading Segments: Current Mode Controllers and Industrial Applications currently dominate the market landscape.

Technology Trends: There is a growing shift toward integrating PWM functionality into System-on-Chip (SoC) designs and developing controllers with higher switching frequencies to allow for smaller overall device footprints.

Competitive Landscape: Industry leaders include Texas Instruments, Analog Devices, STMicroelectronics, Infineon, and ON Semiconductor, all of whom are focusing on geographic expansion into the high-growth Asia-Pacific region.

Get Full Report Here: Pulse Width Modulation (PWM) Controllers Market, Global Business Strategies 2025-2032 - View in Detailed Research Report

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=122483

#Semiconductors #PWMControllers #PowerManagement #TechTrends2026 #ElectricVehicles #DigitalTransformation #EnergyEfficiency #IndustrialAutomation #ElectronicsIndustry #MarketResearch #SemiconductorInsight

Global PWM Controllers Market Set to Reach USD 13.1 Billion by 2032, Driven by Electrification and Digitalization Trends

The global Pulse Width Modulation (PWM) Controllers Market is positioned for steady growth, projected to rise from USD 8.8 billion in 2024 to USD 13.1 billion by 2032, reflecting a CAGR of 6.0%. According to a report by Semiconductor Insight, this expansion is primarily fueled by the twin forces of global electrification and digitalization.

PWM controllers are essential silicon components that regulate power delivery with high efficiency by rapidly switching current on and off. Their ability to minimize heat loss while providing precise voltage control makes them indispensable in the modern transition toward energy-conscious technology.

Key Market Highlights:

Primary Drivers: The shift toward Electric Vehicles (EVs), the rollout of 5G telecommunications, and the rise of intelligent industrial automation.

Leading Segments: Current Mode Controllers and Industrial Applications currently dominate the market landscape.

Technology Trends: There is a growing shift toward integrating PWM functionality into System-on-Chip (SoC) designs and developing controllers with higher switching frequencies to allow for smaller overall device footprints.

Competitive Landscape: Industry leaders include Texas Instruments, Analog Devices, STMicroelectronics, Infineon, and ON Semiconductor, all of whom are focusing on geographic expansion into the high-growth Asia-Pacific region.

Get Full Report Here: Pulse Width Modulation (PWM) Controllers Market, Global Business Strategies 2025-2032 - View in Detailed Research Report

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=122483

#Semiconductors #PWMControllers #PowerManagement #TechTrends2026 #ElectricVehicles #DigitalTransformation #EnergyEfficiency #IndustrialAutomation #ElectronicsIndustry #MarketResearch #SemiconductorInsight

0 Comments

0 Shares

34 Views

0 Reviews